Prices remain firm as planting gets underway. The initial USDA Prospective Plantings report just published this week has a much rosier picture than the industry is currently projecting. The table below shows that the total long grain production is expected to be 99% of last year’s total. The industry is predicting a 10-15% decline, or acres looking much closer to 1.65 million acres. This lower acreage number would appear to be baked into paddy prices right now, which are holding firm across all regions despite scant offshore demand. Louisiana is the only region that is expected to gain acres with any significance, and the rest are expected to taper.

Looking at Medium Grain, the big drop will be coming from drought-plagued California. The USDA is projecting a 315,000 acre medium grain crop from the west coast, but recent water allocations coming out of GCID, the State’s largest water district, are dismal. Initial signals are showing that acreage could fall well below even a 270,000 acre level. Medium grain across the rest of the states will hold relatively constant. It will be interesting to watch planting progress as the weeks tick by and the actual numbers come to light.

As far as planting goes, Louisiana has crested the 60% planted now, approaching as high as 70%. Texas is now approximately nearly 50% planted as well, though rain has slowed progress there a bit last week. They are itching to get started in Arkansas, and we expect to have first plantings by this time next week.

The March rice stocks report was released this week, showing rough rice stocks in all positions down by 8% from this time last year. To break things out, long grain rough is down by 11%, and long grain milled almost 6% down, medium rough about equal, and medium grain milled rice stocks down nearly 40%.

In Asia, Thai prices firmed slightly up to $415pmt, and Viet prices softened just a bit to come down to $415pmt. This is largely based on currency fluctuations and strong demand coming out of China and the usual suspects like the Philippines. India is still holding at steady at $365pmt, and Pakistan is coming in just below at $360pmt.

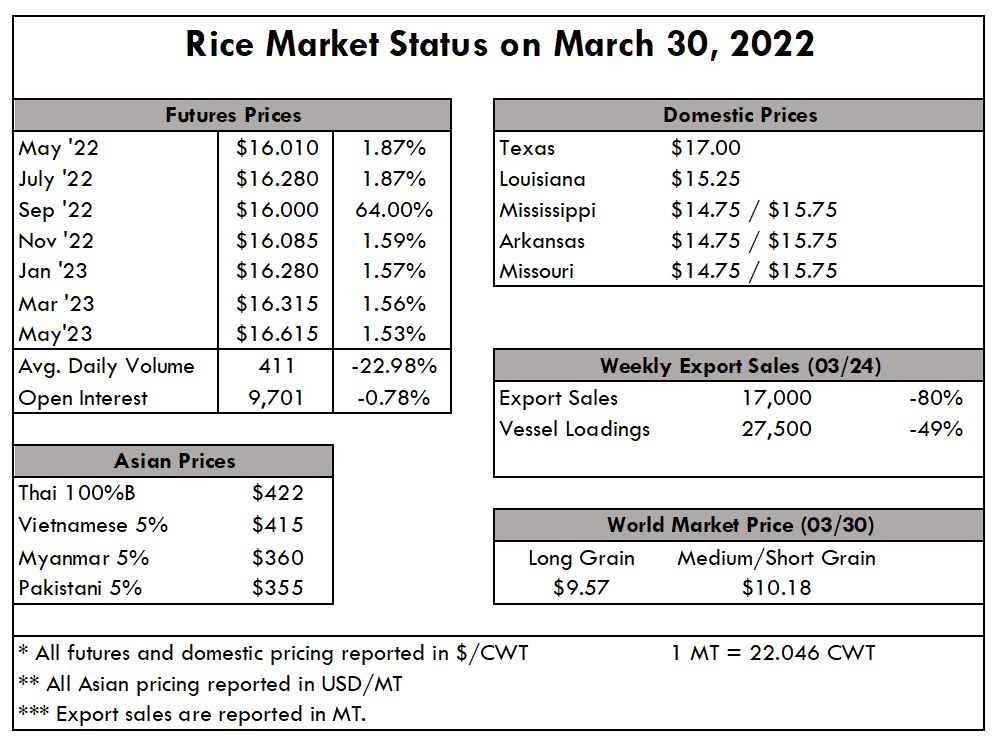

The weekly USDA Export Sales report shows net sales of 17,000 MT for this week, down 80% from the previous week and 71% from the prior 4-week average. Increases were primarily for Guatemala (5,500 MT), Honduras (3,500 MT, including decreases of 400 MT), Mexico (3,300 MT), Canada (2,600 MT), and Saudi Arabia (800 MT). Exports of 27,500 MT were down 49% from the previous week and from the prior 4-week average. The destinations were primarily to Guatemala (11,000 MT), Honduras (6,000 MT), Canada (3,300 MT), Mexico (2,700 MT), and Jordan (1,600 MT).

The month of November showed significant growth for USRPA's Facebook page in our North African Market, RizAmerican. The page gained a total of 1,300 new followers (a growth of 39.3%), with total followers now reaching 4,800. Facebook likes, comments and interaction rates also show positive growth. More than 650,000 impressions were made in just one month, the majority of the audience being females from Tunisia.

Our Moroccan-based influencer @MouniaSenhaji posted a series of stories talking about U.S. rice and prepared a healthy rice salad for her fans in North Africa. She tagged USRPA on Facebook, which also helps to increase awareness and achieve a higher reach, connecting both channels. The stories reached an average of 17,000 accounts per story.

The House and Senate passed legislation to suspend additional cuts to mandatory programs and initiate the process of raising the debt ceiling. The bill delays any additional sequestration cuts to Medicare, farm programs, and other mandatory spending programs and limits Senate debate on a separate debt ceiling increase bill, bypassing the legislative filibuster rules.

Congress will need another bill that would increase the debt limit to ensure the federal government doesn’t exceed its statutory borrowing limit and default. Congress is expected to swiftly draft and pass this legislation ahead of the December 15 deadline set by the Treasury Department.

This week, the USDA released the December WASDE report which contained only minor revisions for both U.S. long-grain and medium & short-grain. The USDA didn’t make any notable changes to the 2020/21 balance sheet in this report but rather focused on the 2021/22 crop. Long-grain imports were revised downward, while export and domestic demand was left steady from the November report. Ultimately, the 2021/22 long-grain carryout was lowered by 1 million cwts, entirely the result of lower imports. Season average farm prices improved, but only slightly, up $0.10 per cwt to $13.10.

Medium & short-grain imports were also lowered this month, but that was more than offset by lower export use which is attributed to higher prices and less supply. The domestic use, as per the norm, appears more resilient against the current market conditions and is even expected to exceed last year’s demand. Ending stocks were assessed up 500,000 cwts, and while California’s price projections are unchanged from last month, southern medium-grain was lowered $0.30 per cwt to $13.70 per cwt.

On the ground, there is little to report in the way of cash trade activity. With tax implications prohibiting some from selling, and the normal holiday slow-down inhibiting others, a more mellow pace is normal for this time of year. However, the market is abuzz with what next year’s acreage numbers will look like as a result of the soaring fertilizer costs and the potential for growers to plant more corn and beans. The expectation is that the largest reduction will come for Arkansas and that Louisiana will remain close to the same as this year. Mississippi and Texas are still up in the air, and California acreage on the West coast is completely contingent on precipitation and the ensuing water policy.

In Asia, prices remain relatively constant. Thai rice remains around $385pmt, Viet at $405pmt, and Indian down at $355. It is notable that Viet prices have dropped in recent weeks to come more in line with Thai prices, while Indian rice has held steady along with their record-breaking export pace.

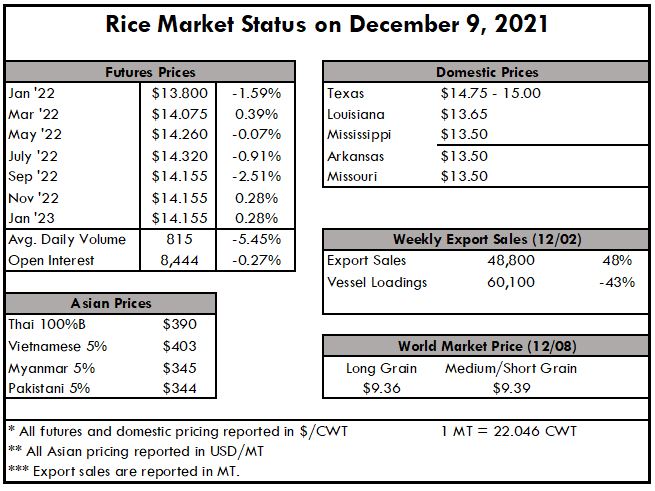

The weekly Export Sales Report shows net sales of 48,800 MT, which is up 51% from last week, but down 22% from the prior 4-week average. Increases were primarily for Honduras (18,500 MT), Guatemala (13,100 MT), Jordan (4,100 MT), Taiwan (3,000 MT), and Canada (2,400 MT).

Exports of 60,100 MT were down 42% from the previous week and 21% from the prior 4-week average. The destinations were primarily to Guatemala (14,400 MT), Japan (13,000 MT), El Salvador (12,400 MT), Haiti (12,400 MT), and Canada (2,600 MT).

Futures have been taking a hit since Thanksgiving, with the low registering this week at $13.79. This could be on account of the cash market being slow, the typical slow-down this time of year, or simply the difficulty in the logistics sector. Average Daily Volume is 815, down 5%, and Open Interest is at 8,444, holding even with last week.

In This Issue:

The US Rice Producers Association Board of Directors held its winter board meeting earlier this week in San Antonio, Texas, primarily focused on strategic planning for 2022 and beyond. Board members also heard trade and legislative updates from the Cornerstone Government Affairs team learned about the positive results of recent USRPA marketing campaigns in Mexico and Central America and met with Foreign Agricultural Service representatives regarding 2022 MAP funding.

Thank you to all our dedicated board members who represent and advocate for their fellow rice producers across the country.

25722 Kingsland Blvd., Ste. 203, Katy, Texas 77494

Phone: 713-974-7423

USRPA does not discriminate in its programs on the basis of race, color, national origin, gender identity, sexual orientation, religion, age, disability, political beliefs, or marital/family status. Persons with disabilities who require alternative means for communication of information (such as Braille, large print, American sign language, language translation, etc.) should contact USRPA at 713-974-7423. EEO.