| The countdown is on. Just 25 days until the Rice Market & Technology Convention (RMTC) 2025 kicks off in vibrant Miami! We're launching the convention with a Networking Welcome Reception on Wednesday, May 28, proudly sponsored by RiceTec. This event sets the tone for the conference, offering a relaxed atmosphere to reconnect with colleagues and forge new partnerships. For more information and to register, visit the official RMTC website.  |

| RMTC2025: Featured Speaker |

|

| RMTC2025: Exhibitor Highlight |

|

|

USDA Highlights President Trump's First 100 Days in Office:

This past Tuesday marked President Trump’s 100th day in office, typically an important checkpoint for any presidential administration. The U.S. Department of Agriculture (USDA) released a press statement highlighting the top issue areas the Department has been working on since Trump was sworn into office. One of the main focal points of the release was USDA’s rollout of the five-point plan to lower the cost of eggs for Americans while simultaneously tackling the highly pathogenic avian influenza (HPAI) outbreak. Additionally, the statement highlighted Rollins' upcoming trade missions to expand markets and boost American agricultural exports, ongoing negotiations with Mexico regarding water treaty obligations, the timely rollout of funds coming out of the Emergency Commodity Assistance Program for the 2024 crop year, and the Secretary’s mission to deliver rural prosperity to Americans. In a similar 100 day memo, USDA highlighted steps taken by each agency to reverse the “woke” Diversity, Equity, and Inclusion (DEI) agenda of the previous Biden Administration highlighting efforts related to freezing funds and grants, revaluation of standing contracts, and the deconstruction of the Partnership of Climate Smart Commodities program. You can find the initial 100-day press release here and the following DEI one here.

USDA Announces Major Win for Agriculture with Regards to Water Negotiations with Mexico: On Monday, USDA Secretary Brooke Rollins announced that an agreement was made between the U.S. and Mexican government for Mexico to meet the current water needs of farmers and ranchers in Texas as part of the 1944 Water Treaty, delivering a huge win for American agriculture. In the agreement, the Mexican government committed to transferring water from international reservoirs and increasing the U.S. share of the flow in six of Mexico’s Rio Grande tributaries through the end of the current five-year water cycle. The agreement between the United States and Mexico solidified a plan for immediate and short-term water relief to meet the needs of Texas farmers and ranchers for this growing season. Additionally, the agreement includes water releases and continued commitments through the end of this cycle, which concludes in October. Under the 1944 Water Treaty, Mexico is obligated to deliver 1.75 million acre-feet over five years to the United States from the Rio Grande River. The United States, in turn, delivers 1.5 million acre-feet of water to Mexico from the Colorado River. Mexico’s persistent shortfalls in deliveries have led to severe water shortages for Rio Grande Valley farmers and ranchers, devastating crops, costing jobs, and threatening the local economy. Going forward, the U.S. welcomes further collaboration with Mexico about their treaty agreements, keeping other outstanding water debts in mind.

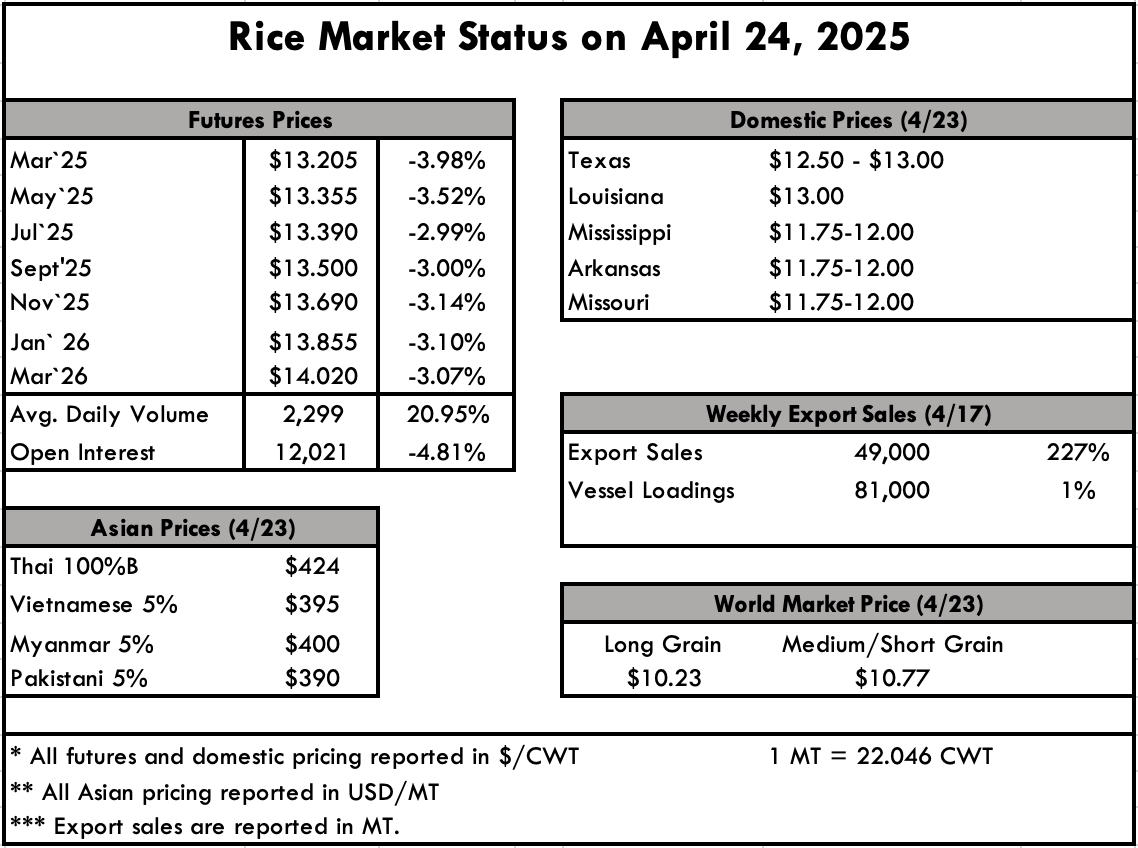

We have been reporting that demand has remained fairly steady, and this is the week where we change our tone; signals in the export market indicate that demand is weakening. Even if mills are busy with old business, selling barges and generating new business is increasingly difficult. The two main culprits are oversupply and poor quality. Having poor quality is a long-term problem that requires attention, but when it’s coupled with multiple replacement options that possess higher quality characteristics at a lower price point (think Mercosur origins), it spells bad news for the short term. One of the only spots to find reprieve right now is the potential for decreased plantings, and the hope for Iraq to come through with a new MOU for the coming year.

The April 28th crop progress report shows that we are still well ahead of the 5-year average in plantings and rice emergence, both up 14% and 11%, respectively. Louisiana is almost finished with 92% planted and 86% emerged, while Texas is just behind at 89% and 77%. Arkansas is 68/40, Mississippi is 62/31, Missouri is 44/11, and California is now at 20/0. Even though we are well ahead of previous years, the anticipated acreage reduction is looking to exceed 200,000 acres in the wake of poor prices and preventative planting. The cutoff date is May 25 for preventive planting in Northeast Arkansas, the most concentrated long-grain producing area in the U.S. Yield loss starts after May 10th, and right now, farmers are saying they need 14 days of dry weather to plant while rain is in the forecast for the days ahead. Estimates of a reduction in long-grain acres are in the 250,000 to 400,000 range.

With the harvest in South America wrapping up, the strong crop and adequate supply will pose a real threat to the U.S. crop being planted right now. While the domestic milled business, Iraq, and Haiti are crucial to the baseline health of the industry and on-farm pricing, so is the paddy export business to our partners in Mexico, Central, and South America. With ample quality supplies in the southern hemisphere to compete with, we do have concerns about pricing when we get to harvest and begin marketing the new crop.

In Asia, prices continue to bounce along the bottom as they have for the past four weeks. There appears to be no shortage anywhere, and even large demand centers like Indonesia are reporting that they won’t be needing as much rice as in the past. Asian prices are nominally quoted at $ 400 pmt, which is nearly a 20% reduction from a year ago. The weekly USDA Export Sales Report shows net sales of 12,700 MT this week, down 74% from the previous week and 62% from the prior 4-week average. Exports of 20,100 MT--a marketing-year low--were down 75% from the previous week and 70% from the prior 4-week average.

The next USDA Export Sales Report will be released on Thursday, May 8, 2025

|

|

| Mark your calendars for the Missouri Rice Research & Merchandising Council's annual Field Day on Thursday, August 14 at the Missouri Rice Research Farm in Glennonville. More details to come this summer! |

Trump names Doug Hoelscher as next USTR Chief Agriculture Negotiator Late last week, it was reported that President Donald Trump plans to nominate Doug Hoelscher as Chief Agriculture Negotiator in the Office of the U.S. Trade Representative (USTR). Hoelscher most recently served as the Chair for the American Leadership Initiative within the American First Policy Institute (AFPI), the Trump-aligned think tank that was founded by U.S. Secretary of Agriculture Brooke Rollins. In addition to his role at AFPI, he is an Iowa native and served in both the George W. Bush and first Trump Administrations in various political roles.

| When one considers the volatility we see in the news and global markets, there is something comforting about steadiness of planting a new crop for the coming year. While the coming campaign will present its own set of challenges, focusing on planting is a welcomed respite from the outside noise. Along that vein, planting is racing along in Louisiana and Texas, where they are 90% and 77% completed, and 80% and 68% emerged. Arkansas is 48% planted and 16% emerged, where Mississippi is 41% and 20%. Missouri is at 18% planted and 7% emerged, while California finally has some rice in the ground at 2%, but nothing emerged. That puts the average plantings at 48%, which is well above the 5-year average of only 9% for this time of year, but behind last year’s pace of 57%. The same trend follows for emergence. The market conditions are largely unchanged, with stable milling taking place on account of domestic business, Iraq fulfillments, and Haitian orders. The fact that we can report things as “stable” is truly a blessing, though it would be nice to see more buying activity. U.S. long grain prices are now quoted closer to $780 pmt (more than double current Indian prices), with Brazilian prices at $575 pmt, Uruguay at $545 pmt and Argentina down to $505 pmt. A recent GAIN report on Paraguay, a growing competitor in the export market, shows that production is forecast up for the 2025/26 marketing year, up to 1.42 MT on a rough basis, or 951,000 MT milled. This is the second highest production level, notching in at just over 538,000 acres. As of mid-April, the harvest was nearly complete with favorable yields and good quality overall. The bottleneck came in the form of infrastructure though, as max acreage is taxing the rice processing system in the form of trucks, intake, and export handling. Exports of 790,000 MT are the third highest, and will supply Brazil, Chile, Costa Rica and other Central American customers. Brazil imports nearly 600,000 MT of the 790,000 MT on a regular basis. Paraguay like its Mercosur neighbors is experiencing its largest harvest in recent years. Yields as high as 9,200 pounds per acre are being reported in numerous areas. The southern Brazilian State of Rio Grande do Sul alone is estimated to have a final paddy harvest of 8.8 million MT. While milling yields are somewhat inconsistent at this time, the overall large production in the four countries may very well total 17 million MT as the final phase of the harvest will soon be completed. As a result prices continue to soften with paddy at an even $300/ton FOB loading port if not lower. Prices in Asia are still bouncing a long the bottom, which after four weeks, is considered a good thing. It would indicate a bottom has been established and the market has adjusted by systematically removing the “unknowns” that accompany a drop. These low prices are a result oversupply, not of the tariffs. Thailand is now reported up from last week at $410 pmt, while Vietnam is steady at $400 pmt, and India is steady at $385 pmt. The weekly Export Sales report shows net sales of 49,000 MT this week, up noticeably from the previous week and up 6% from the prior 4-week average. Increases were primarily for Honduras (13,300 MT), Mexico (12,700 MT), Saudi Arabia (3,100 MT), and Jordan (1,400 MT). Exports of 81,000 MT were up 1% from the previous week and 20% from the prior 4-week average. The destinations were primarily to Mexico (34,100 MT), Honduras (18,000 MT), Haiti (15,200 MT), Japan (4,200 MT), and Saudi Arabia (2,800 MT). |

|

25722 Kingsland Blvd., Ste. 203, Katy, Texas 77494

Phone: 713-974-7423

USRPA does not discriminate in its programs on the basis of race, color, national origin, gender identity, sexual orientation, religion, age, disability, political beliefs, or marital/family status. Persons with disabilities who require alternative means for communication of information (such as Braille, large print, American sign language, language translation, etc.) should contact USRPA at 713-974-7423. EEO.