he Texas Rice Council held a board of directors meeting on October 10 at Midway Bar-B-Q, in Katy, Texas. The Rice Council is entrusted with producer check-off dollars earmarked for promotion, education, and market development. Leaders from academia and the U.S. Rice Industry spoke on topics essential to bettering the Texas Rice Industry. Great turnout with Texas Rice Council board members, USRPA staff and USRPA industry members. |

Dr. Jake Mowrer, Texas A&M Extension Associate Professor in Soil and Crop Sciences, discussed a new sustainability grant regarding nitrogen's importance for rice growth and development. For more information click here. |  Dennis DeLaughter gave an update on the 2023 Market Plan. Dennis DeLaughter gave an update on the 2023 Market Plan. |

Panel discussion and update about the Market Development program. Past, present, and future market developments were discussed. Left to right: Marcela Garcia, USRPA President and CEO; Tommy Turner, Texas Rice Council President, and USRPA Board member; Neal Stoesser, USRPA Chairman; Dennis DeLaughter, Texas Rice Council & USRPA Board Member and Galen Franz, Texas Rice Council & USRPA Board Member. |  Luiz Antonio Michelini, from Agrocete, a Brazilian multinational that operates in the biological, nutrition & plant physiology, and application technology market, spoke to the attendants about the possibility of assistance in evaluating some products in 2024. For more information, you can contact him at luiz.michelini@agrocete.com |

From left to right: Chris Lee, President, Black River Commodities; Dwight Roberts, USRPA Advisor; Harvey Mendoza, Grain Purchasing Manager, Walmart Nicaragua; Mollie Buckler, USRPA Chief Operating Officer; and Roger Gilmore, General Manager, Black River Commodities.Last week, US Rice Producers Association hosted a reverse trade mission for Walmart Nicaragua. The week-long trip through rice country included stops in Texas, Louisiana, Arkansas, and Missouri. Harvey Mendoza, Grain Purchasing Manager for Costa Rica and Nicaragua, represented the company on the trip. From left to right: Chris Lee, President, Black River Commodities; Dwight Roberts, USRPA Advisor; Harvey Mendoza, Grain Purchasing Manager, Walmart Nicaragua; Mollie Buckler, USRPA Chief Operating Officer; and Roger Gilmore, General Manager, Black River Commodities.Last week, US Rice Producers Association hosted a reverse trade mission for Walmart Nicaragua. The week-long trip through rice country included stops in Texas, Louisiana, Arkansas, and Missouri. Harvey Mendoza, Grain Purchasing Manager for Costa Rica and Nicaragua, represented the company on the trip.The trip gave Mendoza an in-depth look at every facet of the U.S. rice industry, from farm to export, with an emphasis on varieties and logistics that might fit the company’s needs. Texas visits at Rice Belt Warehouse, Nutrien, RiceTec, and East Bernard Rice Marketing primarily focused on examining various varieties and taste testing at every nearly every stop. In Louisiana, the group toured the brand-new South Louisiana Rice Mill and an discussed the South Louisiana Rail Facility’s capabilities. In Arkansas, the group visited with Poinsett Rice and Grain and Black River Commodities. Finally, in Missouri, the group visited Inland Cape Rice, another relatively new mill; Wheeler Farms, where they looked at on-farm storage and graded a sample; and Castor River Farms, where they discussed export possibilities. The reverse trade mission was made possible by USDA Market Access Program funding. “The trade mission is the perfect example of the public/private partnerships made possible by MAP funding,” Marcela Garcia, USRPA President & CEO, said. “This kind of trip is what makes a possible purchase go from an idea to reality. We’re happy to be the partner who helps make it happen.” Learn more about USDA’s Market Access Program here. |

During a taste test, Harvey Mendoza visits with Dr. Paola Andrea Mosquera, Senior Breeder at Nutrien. |  Harvey Mendoza and Johnny Hunter, Founder of Castor River Farms near Dexter, MO. |

Harvey meets with Mark Pousson at the South Louisiana Rail Facility and Mill in Lacassine, LA. |  A variety overview with Jay Davis of East Bernard Rice Marketing and USRPA Board Member Tommy Turner in East Bernard, TX. |

| The USDA’s WASDE was published this week, sending a bullish signal into the U.S. rice world by dropping carryover by 1.3 million cwt, or 5%. Last month’s report called for 24.1 million cwt of carryover, while this month it calls for only 22.8 million cwt on increased exports. The new crop export forecast was raised by 1 million cwt to 86 million for long grain rice because of strong early sales to Mexico, Central America, and Iraq. Also of note is a decrease of 14 pounds/acre in the forecast yield for the U.S. rice harvest; we will know more about the field and milling yields within the month. The global outlook from the WASDE is sideways, calling for increased supplies, consumption, and trade right in line with last month. Ending stocks on a global scale are largely unchanged, resting at 167.5 million tons, which remains the lowest level in six years. The October FAO rice price index reported an average of 141.7 points for September, a drop of 0.5% from August, though still 25% higher than this time last year. This slight decline came from Japonica and Aromatic prices, where full crops in California and the southern U.S., along with strong supply from Australia resulted in medium grain indexes dropping 11%. On the broader long grain market, however, those prices through September sustained their post-Indian export ban pricing with Vietnam and Thailand both sourcing rice for prices in excess of $600 pmt. We expect to see the FAO index drop significantly in next months’ report, as the broader Indica market has settled down, and is currently trading now below $600 pmt. On a calendar year, it is nice to see that Iraq is helping to pick up the slack from exports to Haiti, Mexico, and Japan. Our top export market through July is Haiti with 208 MT, followed by Mexico at 184 MT and Japan with 158 MT. Last year through the same period, Mexico was on top with 352 MT, then Haiti with 264 MT, and Japan with 205 MT. The difference maker is that Iraq has 132 MT this year, whereas they had zero last year. A strong harvest and resulting supply will help the export figures bounce back to these key markets, as well as to some of our smaller markets in the coming months. With Mercosur largely out of the market until the new harvest, paddy importers are focused on the U.S. supply. Over the past few weeks, the US Rice Producers Association has hosted buyers visits from Ecuador, Mexico, Guatemala, Nicaragua, and Guyana while numerous others in the Western Hemisphere have inquired about the U.S. crop. The low level of the Mississippi River is a concern that has the attention of export merchants and buyers.  South Louisiana Rail Facility continues an active export season with the loading of the above vessel destined for Mexico with 25,000 tons of rough rice. In Asia, another tender from BULOG, Indonesia’s rice purchasing arm, has kept Viet and Thai markets rolling. At the start of the year, Indonesia was expected to procure no more than 2 MMT. But as the bans in India unfolded and climate risk shined a light on food security, the country has taken major steps and is expected to amass nearly 4 MMT of rice this year, fully doubling the originally anticipated purchases. While this is all rice that will come from the Far East, it keeps pressure on already high global prices and helps to buoy prices in the Western Hemisphere. On the back of BULOG’s announcement to procure more rice, Viet prices jumped back up to $615 pmt, nearly $35 pmt over Thai prices, currently at $585 pmt. The one wild card that could come to fruition is a G2G deal between India and Indonesia, which could soften prices out of Vietnam and the entire complex. If we see that happen, it could be the prelude to a relaxing or complete removal of the export ban. |

|

President Biden signs continuing resolution into law: On Saturday, the White House announced President Biden had signed into law H.R. 5860 – “A bill making continuing appropriations for fiscal year 2024 and for other purposes.” It was introduced in the House on Saturday, the last day of fiscal year 2023, and quickly moved through both chambers to avert a government shutdown. The bill provides funding for the federal government through November 17 and includes $16 billion in supplemental funding for domestic disaster relief; however, none of the disaster relief in the bill will go through the Department of Agriculture, though funding could support Federal Emergency Management Agency work in rural and agricultural communities impacted by hurricanes, floods, or other declared disasters. The bill extends the funding provided in the fiscal year 2023 agriculture appropriations bill at the same spending levels provided in that bill but prorated only through November 17. The bill did not address any farm bill programs, some of which expired on September 30. Neither the House nor Senate have introduced a bill to reauthorize the farm bill yet.

USRPA hosted Harvey Mendoza, Deputy Manager for Grain Purchasing for Walmart Nicaragua, on a Reverse Trade Servicing trip this week. The trip included stops in Texas, Louisiana, Arkansas, and Missouri. Here the group meets with Rice Belt Warehouse team in El Campo, Texas. More to come in next week's issue of The Rice Advocate. |

| Harvest marches on with strong progress this week across all rice states. Arkansas jumped to over 80% complete — nearly 10% ahead of last year and the 5-year average—while Louisiana, Mississippi, and Texas are all but complete. Missouri is on the back-half of their harvest, while the Californians have finally hit full-stride, registering at 20% complete as a state. There are minor weather events on the horizon, and a deluge of rain in some regions this week that caused a lot of rice to go down, but optimism reigns on the west coast for a solid harvest. Last week we reported on high field yields and low milling yields in Arkansas… and the story is the same this week. Producers are ecstatic about what their yield monitors are displaying in the field, but we can state with moderate confidence that head rice is going to average about 50 lbs this year, perhaps a bit higher. With the large acreage and high yields, the bottle-neck for some regions in Arkansas and Mississippi could turn out being the waning flow of the mighty Mississippi. Low precipitation levels and low river flows are causing concern in the logistics chain; more to report here as the situation develops. The cash and futures market has been slow to materialize this year. The expectation was that we would be further along in market direction this deep into harvest, but the whiplash from India’s export ban and ensuing market reaction has resulted in significant caution from buyers. This doesn’t mean they aren’t coming to market, but simply that they are covered for the moment and want more information before booking business or taking any sizable positions. We do know that U.S. prices are very competitive with South American prices, and exporters south of the border don’t have sizable supplies. Paddy sellers want and expect higher prices, but the confidence to sell a milled (or paddy) product on the export market is not there yet. Again, U.S. long grain is in the $755-$765pmt range, Uruguay at $745, Argentina $740, and Brazil $715. The tables have certainly turned when comparing this year to last year. Spring planting is well underway in Mercosur countries and a large crop is anticipated. The Paraguayan harvest will begin in January. In Asia, we have seen a significant cooling with the panic all but gone, and perhaps now with enough perspective to process what this market might look like when India re-enters the market. It might be too early to talk about the nuts-and-bolts of this action, but we all know it’s coming. Remember the ban was instituted in September on the assumption the El Niño would severely reduce the crop size. Well, we are almost through the season and the numbers won’t lie. In any case, Vietnam has held firm in the $610 pmt range, Thailand at $595 pmt, and Pakistan in the $550 pmt range. Remember that before the ban, prices were hovering right around $500 pmt. The weekly USDA Export Sales report shows net sales of 53,100 MT this week, up 89% from the previous week and 10% from the prior 4-week average. Notably, Nicaragua registered for 25,000 MT. Exports of 25,500 MT were down 45% from the previous week and 48% from the prior 4-week average. |

|

| FSA announces second payment through the Rice Production ProgramLast Friday, the USDA Farm Service Agency (FSA) announced that eligible rice producers who received an initial program payment through the Rice Production Program would receive an additional payment of .28 cent per pound. Recipients will not be required to submit a new application and payments will be determined on previously reported data. The Consolidated Appropriations Act of 2023 provided USDA with the authority and funding to provide up to $250 million in assistance to rice producers to counter stagnant prices and high input costs during the 2022 crop year. Earlier this year, FSA provided payments to producers totaling $195 million under a payment rate of 1 cent per pound. House considers agriculture appropriations bill amendments this week, the full House considered the appropriations bill for USDA and the Food and Drug Administration for fiscal year 2024. The House considered and adopted amendments to the bill, many of which further reduced spending in the bill. Final passage of the bill is uncertain at this time due to concerns from members on the bill’s overall reduced spending levels and inclusion of a policy related to mifepristone. The current fiscal year concludes on September 30 and barring passage of a continuing resolution by both chambers, a government shutdown will commence on October 1. As of Thursday afternoon, the Senate has introduced and moved forward with procedural steps on a continuing resolution to fund the government through November 17. While proposals for a continuing resolution have been introduced in the House, the chamber has yet to consider any legislation to fund the government for the short term. |

| Organized by the US Rice Producers Association, five rice mills from Ecuador and three government officials spent a week in the Mississippi River Delta from St. Louis to New Orleans, visiting every aspect of the U.S. rice trade. The purpose of the trip was to gain a solid understanding of how rice is grown and handled from the field to an ocean vessel for export. The last time Ecuador imported rough rice from the United States was in 1997 due to an El Niño weather phenomenon. Since that year Ecuador has been self-sufficient in rice and most years have had a surplus that could be exported to neighboring markets. Due to a long-time relationship between the USRPA and Ecuador’s CORPCOM (Corporacion de Industriales Arroceros del Ecuador), the national rice millers organization, the two groups began discussions earlier in the year about the market and the supply/demand issues in the Western Hemisphere. Aware of meetings in Ecuador between the rice mills, producers, and the Ministry of Agriculture, the USRPA invited CORPCOM members and government officials. After 1997 Ecuador had not been involved in the rice trade outside of their country. That year the population totaled 11 million but today the population has grown to 18 million, putting increased pressure on production where average yields are 5,500 pounds per acre. The visit to the delta by five mills and two government officials was an overwhelming success as noted by their comments. “Thank you for all your attention, you made a week of work like a vacation, meeting great people and professionals.” “Thank you very much for organizing and sharing your experience and knowledge with us, an enriching trip." ”You made us feel as if we were at home and we could verify every step in the process chain of rice, where we could resolve our concerns.” |

A glimpse of harvest and a conversation with Justin and Landon Wheeler at Wheeler Farms near Grayridge, MO. A glimpse of harvest and a conversation with Justin and Landon Wheeler at Wheeler Farms near Grayridge, MO. |  A market presentation at Bunge headquarters in St. Louis kicked off the week. A market presentation at Bunge headquarters in St. Louis kicked off the week. |

The group met with USDA - Federal Grain Inspection Service staff in Stuttgart, AR. The group met with USDA - Federal Grain Inspection Service staff in Stuttgart, AR. |  Thanks to Dr. Jarrod Hardke and his team at the Arkansas Rice Research and Extension Center for hosting the group for lunch. Thanks to Dr. Jarrod Hardke and his team at the Arkansas Rice Research and Extension Center for hosting the group for lunch. |

TRC Group and Russell Marine Group hosted a grading workshop for the group. TRC Group and Russell Marine Group hosted a grading workshop for the group. |  A river tour and export logistics discussion with Russell Marine Group in New Orleans. A river tour and export logistics discussion with Russell Marine Group in New Orleans. |

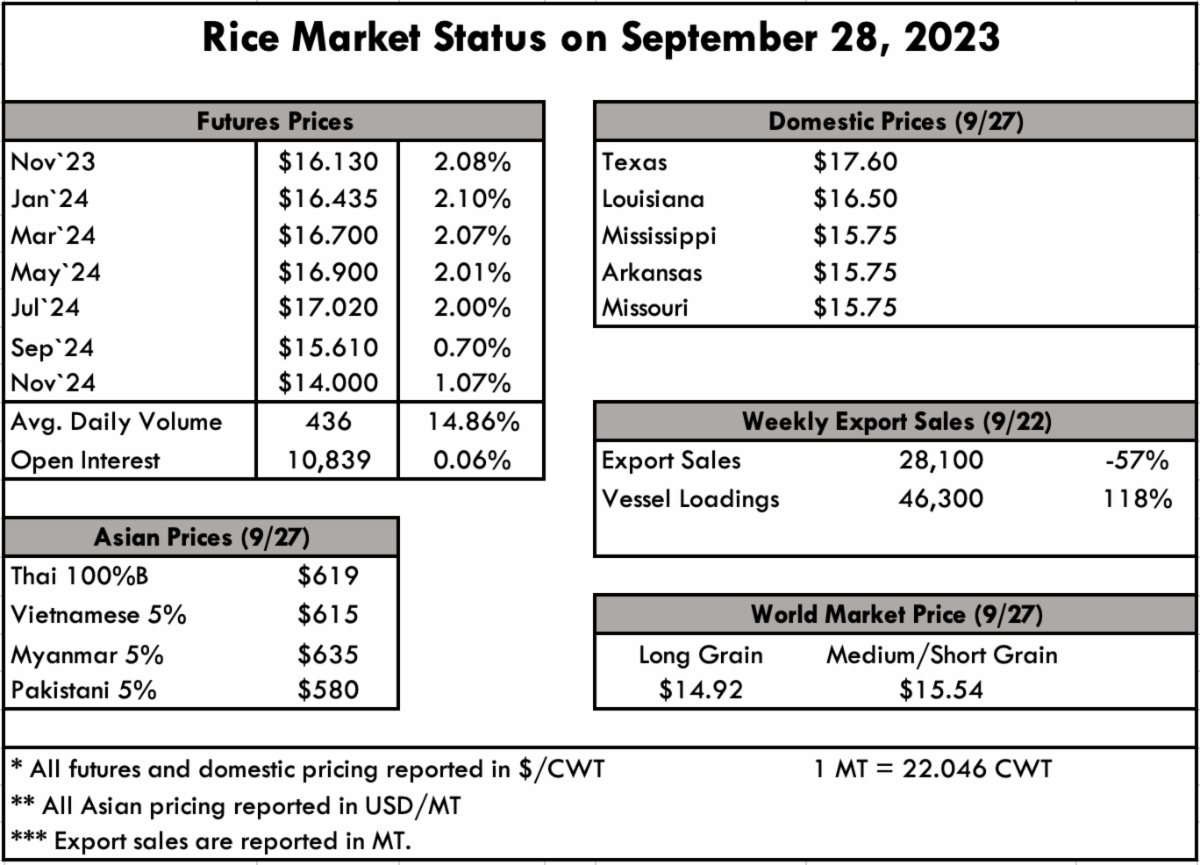

| Milling yields are the only thing that’s lacking this harvest. We are ahead of pace, up on acres, and up on yields almost across the board, but converting the ample paddy supply to an ample milled product is proving more difficult than anticipated. While this isn’t a huge surprise to anyone because of the excessive heat at key times throughout the growing season, it’s about the only negative we can cite at the moment — which is a net positive! Export prices are competitive with South American origins, and we are largely isolated from any negative impacts of the Indian export bans. In actuality, we are a beneficiary because Iraq took swift action to book milled rice from the U.S., and mills are busy through the end of the year filling that business. Last year all we could report was the doom and gloom of negative food policies foreign governments were taking to combat raging food inflation to the detriment of our U.S. long grain crop. This year represents a new opportunity, in which we will be a featured and stable supplier of long grain rice. Let’s just hope the milling yields improve, as this will be the year we can gain some of our market share back from our drought-stricken South American competitors, namely Brazil. On the ground, prices in Texas are holding at $17.60/cwt, while Louisiana is at $16.50/cwt. Mississippi, Arkansas, and Missouri are in the $15.75/cwt range. The futures market is also firming up a bit, 2%+ increases from Nov '23 thru Jul ’24, with Jul ’24 registering as high as $17.020. Average daily volume jumped 14.86% up to 436, while open interest held steady at 10,839 this week. The USDA crop progress report shows the entire complex at 66% complete, 7% above the 5-year average. Louisiana is leading the charge with 95% complete, followed by Texas at 92%, Mississippi at 90%, Arkansas at 70%, Missouri at 53%, and California at 10%. Arkansas is 1% ahead of last year, and California is 8% behind last year. In Asia, stability has returned with prices settling in Thailand and Vietnam between $600-$610 pmt. India is still the driver in the region, but with small announcements surfacing of approved G2G deals (Saudi Arabia) an adjusting market, a “business as usual” is returning. In the Western Hemisphere, all prices are now exceeding $700 pmt, with Brazil around $715 pmt, Argentina at $740 pmt, Uruguay at $745-750 pmt, and the U.S. at $755-$765 pmt. The difference here is that the U.S. is the only origin with legitimate supplies until March when the Southern Hemisphere harvest is underway. With prices this firm in the long grain market, it will be interesting to see the medium grain acres planted next year. It’s too early to tell now, but by February when seed is booked and planting decisions are made, we would forecast a drop in medium grain acres and a return to long grain by some degree. The weekly USDA Export Sales report shows net sales of 28,100 MT, 57% down from the previous week and 55% down from the prior 4-week average. Increases primarily for Haiti (15,100 MT, including decreases of 100 MT), Honduras (9,500 MT), Canada (2,000 MT), Belgium (500 MT), and Israel (400 MT), were offset by reductions for Guatemala (400 MT). Exports of 46,300 MT were up noticeably from the previous week, but down 13% from the prior 4-week average. The destinations were primarily to Japan (26,000 MT), Haiti (15,100 MT), Canada (2,100 MT), Mexico (1,900 MT), and Belgium (500 MT). |

|

| Market Update: Milling Yields Down, But Pace and Acres Up |

| Milling yields are the only thing that’s lacking this harvest. We are ahead of pace, up on acres, and up on yields almost across the board, but converting the ample paddy supply to an ample milled product is proving more difficult than anticipated. While this isn’t a huge surprise to anyone because of the excessive heat at key times throughout the growing season, it’s about the only negative we can cite at the moment — which is a net positive! Export prices are competitive with South American origins, and we are largely isolated from any negative impacts of the Indian export bans. In actuality, we are a beneficiary because Iraq took swift action to book milled rice from the U.S., and mills are busy through the end of the year filling that business. Last year all we could report was the doom and gloom of negative food policies foreign governments were taking to combat raging food inflation to the detriment of our U.S. long grain crop. This year represents a new opportunity, in which we will be a featured and stable supplier of long grain rice. Let’s just hope the milling yields improve, as this will be the year we can gain some of our market share back from our drought-stricken South American competitors, namely Brazil. On the ground, prices in Texas are holding at $17.60/cwt, while Louisiana is at $16.50/cwt. Mississippi, Arkansas, and Missouri are in the $15.75/cwt range. The futures market is also firming up a bit, 2%+ increases from Nov '23 thru Jul ’24, with Jul ’24 registering as high as $17.020. Average daily volume jumped 14.86% up to 436, while open interest held steady at 10,839 this week. The USDA crop progress report shows the entire complex at 66% complete, 7% above the 5-year average. Louisiana is leading the charge with 95% complete, followed by Texas at 92%, Mississippi at 90%, Arkansas at 70%, Missouri at 53%, and California at 10%. Arkansas is 1% ahead of last year, and California is 8% behind last year. In Asia, stability has returned with prices settling in Thailand and Vietnam between $600-$610 pmt. India is still the driver in the region, but with small announcements surfacing of approved G2G deals (Saudi Arabia) an adjusting market, a “business as usual” is returning. In the Western Hemisphere, all prices are now exceeding $700 pmt, with Brazil around $715 pmt, Argentina at $740 pmt, Uruguay at $745-750 pmt, and the U.S. at $755-$765 pmt. The difference here is that the U.S. is the only origin with legitimate supplies until March when the Southern Hemisphere harvest is underway. With prices this firm in the long grain market, it will be interesting to see the medium grain acres planted next year. It’s too early to tell now, but by February when seed is booked and planting decisions are made, we would forecast a drop in medium grain acres and a return to long grain by some degree. The weekly USDA Export Sales report shows net sales of 28,100 MT, 57% down from the previous week and 55% down from the prior 4-week average. Increases primarily for Haiti (15,100 MT, including decreases of 100 MT), Honduras (9,500 MT), Canada (2,000 MT), Belgium (500 MT), and Israel (400 MT), were offset by reductions for Guatemala (400 MT). Exports of 46,300 MT were up noticeably from the previous week, but down 13% from the prior 4-week average. The destinations were primarily to Japan (26,000 MT), Haiti (15,100 MT), Canada (2,100 MT), Mexico (1,900 MT), and Belgium (500 MT). |

|

DHS releases proposed rule for H-2A program

On Wednesday, the Department of Homeland Security (DHS) released a notice of proposed rulemaking to increase oversight of its H-2 temporary visa program, including for workers in the H-2A temporary agricultural program. The proposed rule would allow H-2A workers to switch to employers that do not use E-Verify to check workers' legal status. DHS is accepting comments on the proposal through November 20. This proposal follows last week’s release of a proposal from the Department of Labor on the H-2A program. Interested parties can view the proposed rule here and submit comments here.

House Committee on the Budget advances budget resolution

On Wednesday, the House Committee on the Budget passed a budget resolution for fiscal years 2024-2033, titled “Reverse the Curse” on a 20-14 vote. The resolution included a policy statement on agriculture, which stated the importance of protecting the farm safety net and curbing the use of the Department of Agriculture’s Commodity Credit Corporation. The full budget resolution can be found here.

25722 Kingsland Blvd., Ste. 203, Katy, Texas 77494

Phone: 713-974-7423

USRPA does not discriminate in its programs on the basis of race, color, national origin, gender identity, sexual orientation, religion, age, disability, political beliefs, or marital/family status. Persons with disabilities who require alternative means for communication of information (such as Braille, large print, American sign language, language translation, etc.) should contact USRPA at 713-974-7423. EEO.